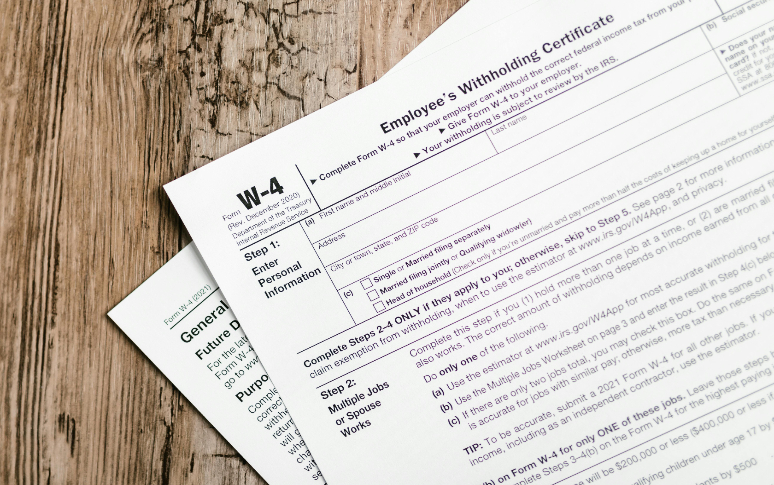

The Basics of Form W-4

Form W-4 tells your employer or employer's payroll representative how much federal income tax withholding to keep from each paycheck. You generally complete Internal Revenue Service (IRS) Form W-4, Employee's Withholding Certificate, at the start of any new job. The form is crucial in determining your balance due or refund each tax season.

You don't have to fill out a new Form W-4 every year as long as you have one on file with your employer. However, it's a good idea to check on your federal withholding annually or if you have any life changes.

When to Update Your W-4

Life changes often require updating your W-4 form. Major events like marriage, divorce, having a baby, or starting a second job can significantly impact your tax situation. Just as you'd update your GPS when taking a new route, your W-4 needs adjusting when your financial journey changes direction. Failing to update your W-4 could result in unexpected tax bills or missed opportunities for larger paychecks.

Your tax withholding accuracy depends on keeping your W-4 current with your life circumstances. For instance, if you recently got married, you might want to adjust your withholding to account for your spouse's income and avoid under-withholding penalties.

Step-by-Step Guide to Completing Form W-4

The first section requires your personal information, including your name, address, and Social Security number. This step also asks for your filing status - Single, Married Filing Jointly, Married Filing Separately, Head of Household, or Qualifying Surviving Spouse. Think of this as creating your tax identity card.

Your filing status significantly affects your tax bracket and standard deduction amount. For example, choosing Married Filing Jointly typically results in lower overall taxes compared to filing separately, but this depends on your specific situation.

Multiple Jobs and Spousal Income Considerations

If you have multiple jobs or your spouse works, you'll need to complete Step 2 of the W-4 carefully. You have three options: use the IRS tax withholding estimator, complete the Multiple Jobs Worksheet, or check the box in Step 2(c) if you have two similarly-paying jobs.

Failing to account for all income sources is like trying to balance your checkbook while only looking at one account - it doesn't give you the full picture. The most accurate method is using the IRS tax withholding estimator, which accounts for all income sources and helps prevent under-withholding.

Claiming Dependents and Tax Credits

Step 3 allows you to claim credits for qualifying children and other dependents. For each qualifying child under 17, you can claim up to $2,000 in credits. Other dependents may qualify for a $500 credit each. Remember, only one spouse should claim these credits on their W-4 to avoid under-withholding.

These credits directly reduce your tax liability, unlike deductions which only reduce your taxable income. For example, if you have two qualifying children, you could potentially reduce your tax liability by $4,000.

Adjustments and Other Income

Step 4 lets you account for additional income, deductions, and extra withholding. This includes income from investments, retirement accounts, or side gigs. You can also factor in deductions like mortgage interest, charitable contributions, or state and local taxes if you plan to itemize.

Consider this section your tax fine-tuning tool. For instance, if you have $5,000 in annual investment income, you might want to include this in Step 4(a) to avoid owing taxes at year-end.

Strategies for Optimizing Your Withholding

You can adjust your W-4 to either increase your take-home pay or boost your tax refund. To get more money in each paycheck, consider claiming applicable deductions in Step 4(b). For a larger refund, you might add extra withholding in Step 4(c).

Think of this like adjusting your thermostat - you're finding the right balance between comfort now (paycheck size) and comfort later (tax refund or payment).

Common Mistakes to Avoid

Many people make the mistake of claiming too many deductions or failing to account for all income sources. Another common error is having both spouses claim the same credits or deductions on their respective W-4s.

These mistakes can lead to unexpected tax bills or penalties. For example, if both spouses claim child tax credits, they might end up owing thousands in taxes due to insufficient withholding.

Next Steps and Recommendations

Review your W-4 annually or whenever you experience significant life changes. Consider consulting with a tax professional if your situation is complex. Keep copies of your completed W-4 forms for your records.

By following these guidelines and regularly reviewing your withholding strategy, you can optimize your paycheck while ensuring you meet your tax obligations. Remember, the goal is to have your withholding match your tax liability as closely as possible to avoid both large refunds and unexpected tax bills.

Was this page helpful? Give us a thumbs up!